Python Quantitative Trading

Python quantitative trading refers to the process of using the Python programming language along with related libraries and tools to analyze financial market data, develop strategies, and execute trades.

Python has become one of the preferred programming languages for quantitative trading due to its simplicity, ease of learning, powerful ecosystem, and rich financial libraries.

Quantitative trading is widely used in the financial field, allowing traders to formulate and execute trading strategies through systematic methods, improving trading efficiency and the scientific nature of decision-making.

Quantitative trading mainly involves using mathematical and statistical methods to perform quantitative analysis of financial markets through computer technology, thereby formulating and executing trading strategies.

For more Python quantitative trading content, see: Python Quantitative Trading.

Example Application

Section titled “Example Application”Let’s first look at a simple Python quantitative trading example using a moving average strategy with Yahoo Finance data.

The basic idea of this strategy is to generate buy and sell signals by comparing short-term and long-term moving averages.

Before running this simple example, you need to install three packages:

Package Description:

- Pandas is a powerful open-source data processing and analysis library, specifically designed for efficient data analysis and manipulation.

- yfinance is a library for fetching financial data, supporting the retrieval of stocks, indices, and other financial market data from Yahoo Finance.

- Matplotlib is a 2D plotting library for creating static, dynamic, and interactive data visualization charts.

Fetching Historical Stock Data

Section titled “Fetching Historical Stock Data”Use yfinance to fetch historical stock data. Here is a simple example:

Example

Section titled “Example”Output result is as follows:

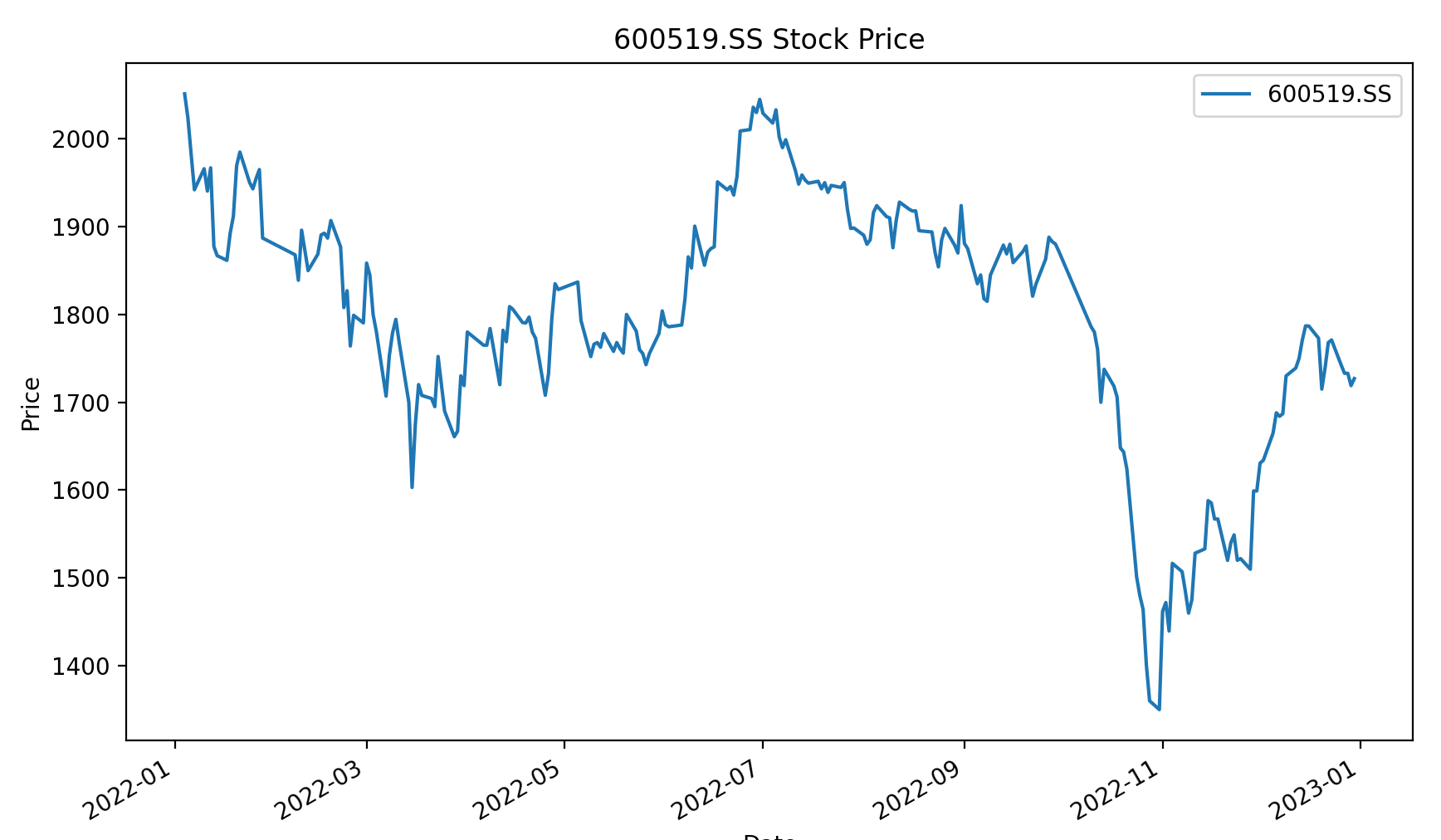

Simple Data Analysis and Visualization

Section titled “Simple Data Analysis and Visualization”Use pandas for data analysis and matplotlib for visualization:

Example

Section titled “Example”The trend chart is displayed as follows:

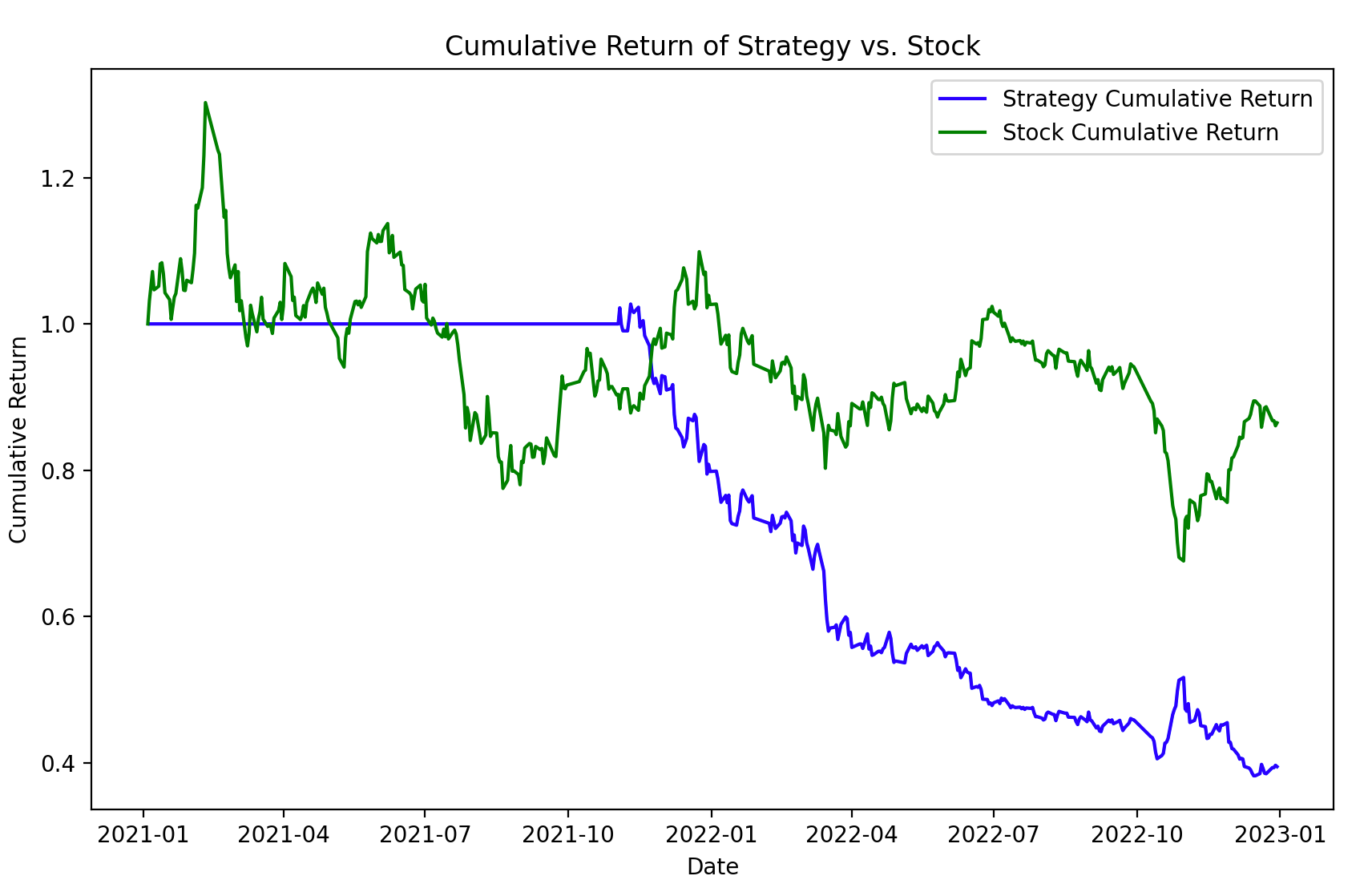

Moving Average Crossover Strategy Backtest

Section titled “Moving Average Crossover Strategy Backtest”Backtesting is the process of simulating and evaluating a trading strategy on historical market data.

The following is an example code for a simple moving average crossover strategy backtest. The strategy buys when the 50-day moving average crosses above the 200-day moving average, and sells when it crosses below. The strategy’s performance is output with indicators such as total return, annualized return, and maximum drawdown.

Example

Section titled “Example”The display chart is as follows:

Please note that this is just a simple example. In practical applications, more complex strategies and more considerations are needed.